1 December 2021

Fuelling the Next Leap in Growth through the Sun Belt and Emerging Markets

Just over five months ago, Manulife US REIT (MUST) organised and invited us for a presentation by Scott Homa and Phil Ryan who are the Senior Director and Director respectively of the Office Research Department at JLL U.S. We covered the details of the presentation which we titled Manulife US REIT: Switching to High-Gear? which gives a good context to the current trends in the U.S. office markets.

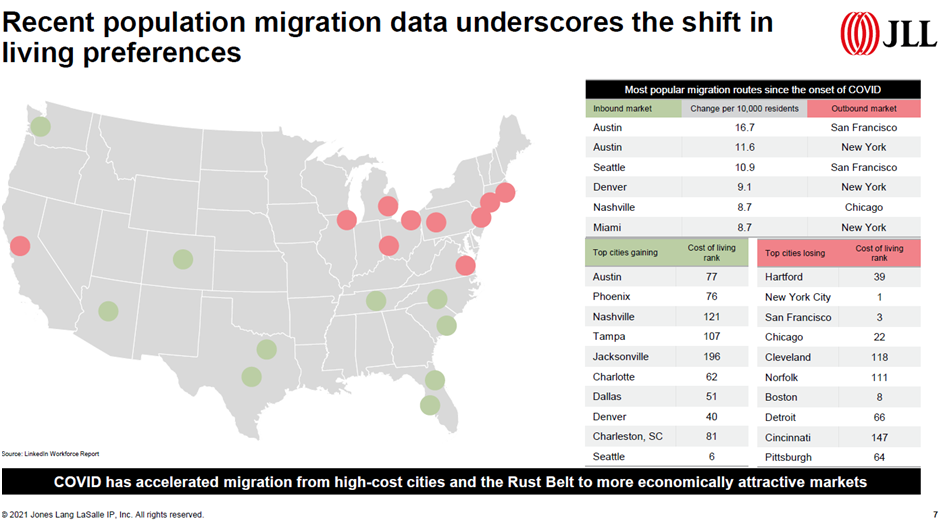

The high-level summary of the sharing session was that there has been a structural trend of domestic migration within the U.S. out from the traditional gateway cities in the East and West Coast (e.g. New York, Boston, Los Angeles, San Francisco, and Chicago) into the Sun Belt states (e.g. Arizona, Florida, Georgia, South Carolina, Southern California, North Carolina, and Utah) and emerging markets (e.g. Austin, Charlotte, Pittsburgh, Phoenix, Nashville, Minneapolis, and Columbus). These migration trends are driven by several factors such as:

- Lower state taxes

- Lower cost of living

- Lower real estate cost

- New job opportunities

- Milder and warmer climates

- Milder COVID-19 movement restrictions

These trends naturally attract corporations to seek a strong and educated talent pool in those regions which drives up office demand and hence rental growth and real estate valuations.

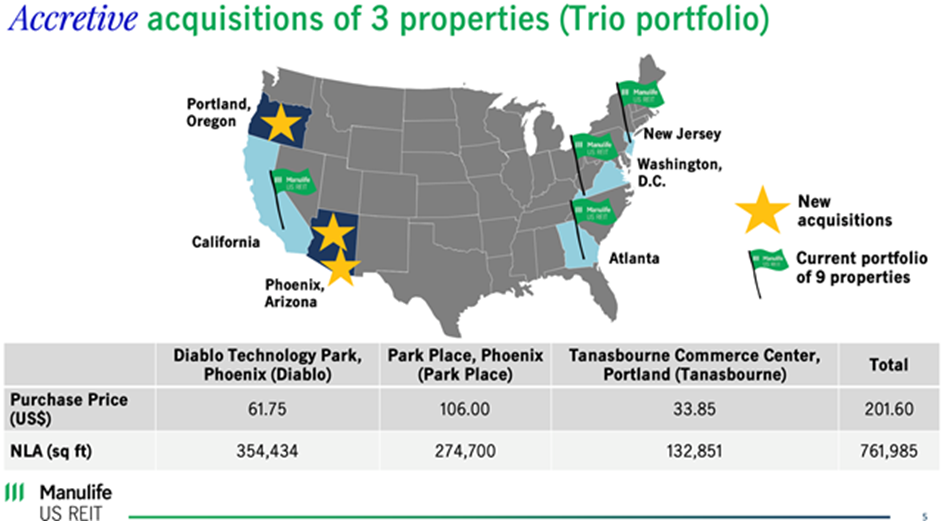

Just yesterday, Manulife US REIT had announced an acquisition of a trio of properties, two in Phoenix, Arizona and one in Portland, Oregon; namely Diablo Technology Park (Tempe), Park Place (Chandler) and Tanasbourne Commerce Center (Hillsboro). This brings the REIT’s portfolio up from 9 to 12 assets.

Source: Manulife US REIT

In this article, we will take a closer look at the assets and the sub-markets that these properties are located in.

Accretive Acquisition at the Heart of Silicon Desert and Forest

Source: Silicon Maps

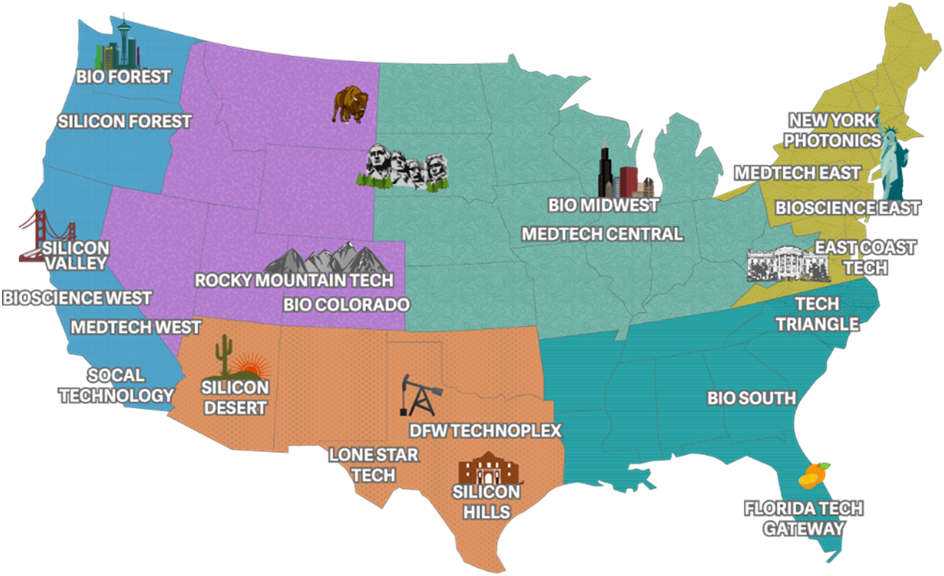

The traditional technology centre of the world was Silicon Valley in San Jose, California. Replicates of the success of Silicon Valley, such as new tech and knowledge hubs sprang up in other U.S. states driven by lower taxes and lower cost of living, for example:

- Silicon Desert: Phoenix, Arizona

- Silicon Forest: Portland, Oregon

- Silicon Harbour: Charleston, South Carolina; Stamford, ConnecticutAustin, Texas

- Silicon Hills: Austin, Texas

- Silicon Slopes: Salt Lake County, Utah

Source: Manulife US REIT

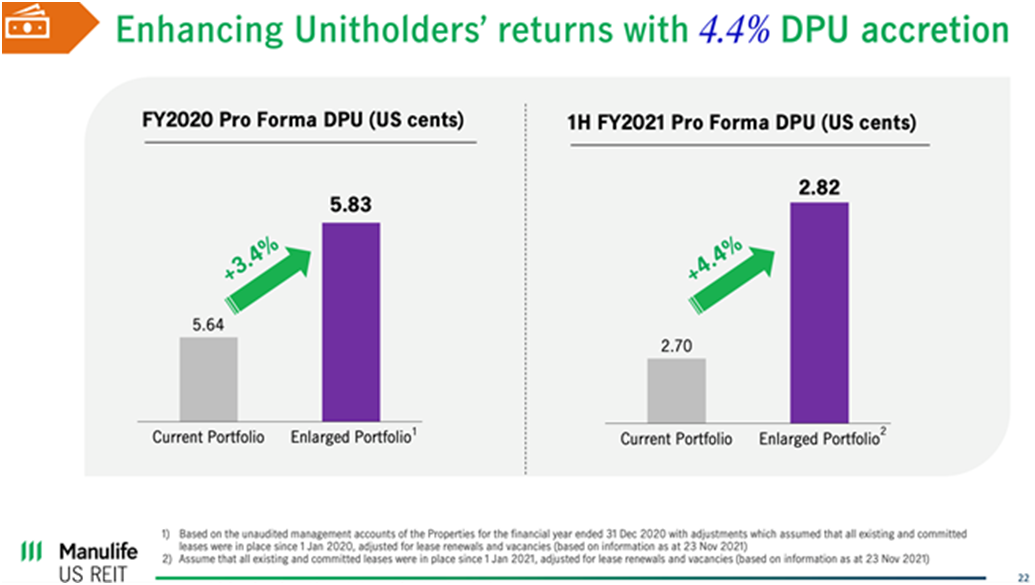

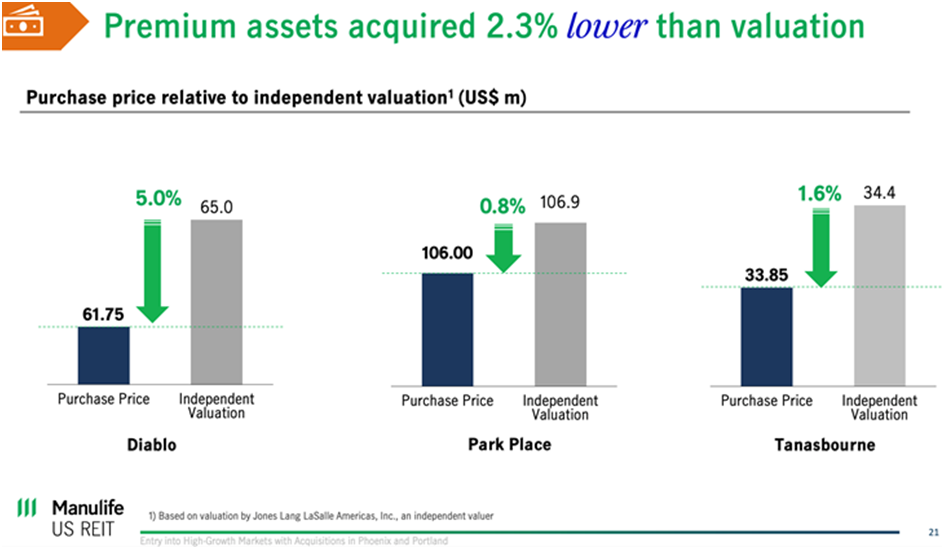

MUST’s new ‘Trio’ portfolio of Diablo Technology Park (Diablo) and Park Place are located in the heart of Silicon Desert while Tanasbourne Commerce Center (Tanasbourne) is in the Silicon Forest. Coupled with a 2.2% blended average discounted acquisition price to the valuation, the acquisition will be immediately 3.4% and 4.4% accretive to the DPU on a pro forma basis based on FY2020 and 1HFY2021 DPU, respectively.

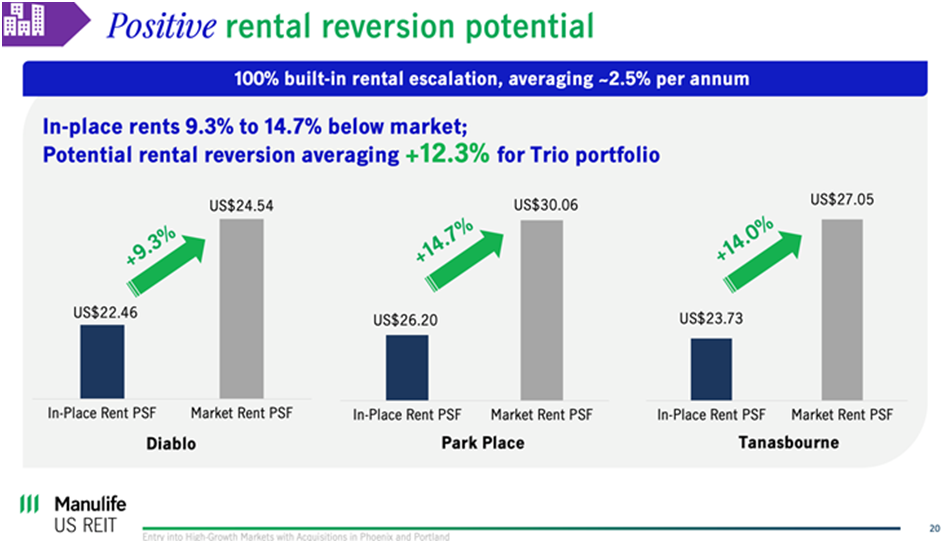

Beyond the immediate accretion, what we think gives this acquisition future growth potential is really the lower in-place rents currently compared to the current market rents in the region. Diablo’s current rental is reported to be approximately 9.3% below the market rents on a per square feet basis while Park Place is reported to be 14.7% below market rents. With a built-in range of 1.0% to 3.0% annual rental escalation of the tenants, this portfolio is expected to compound its rental revenue at an average rate of 2.5% annually.

The usual concern is the tenancy contract “break-clauses” which could derail this long-term and predictable compounded growth through the rental escalations. MUST has clarified that while “break-clauses” do exist in the lease contracts, premature termination carries a fairly hefty compensation of between 12 to 14 months of rental, thus reducing the risk to the REIT.

Source: Manulife US REIT

Source: Manulife US REIT

A Positive Departure – Class-A Tenants in Class-B Buildings

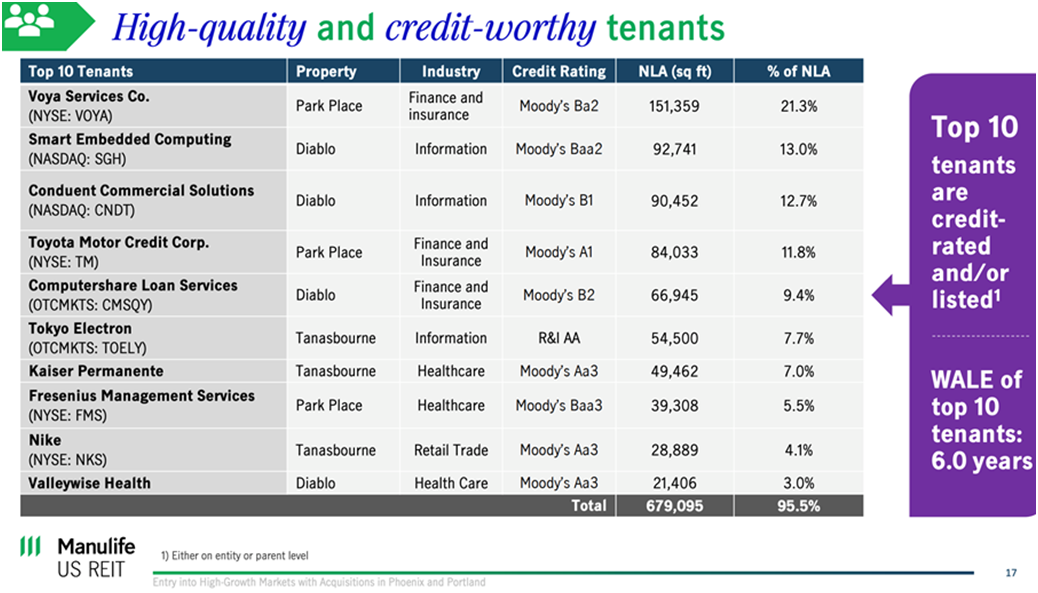

This recent acquisition announcement from MUST represents a departure from its long-established strategy of going after Class-A and Trophy assets in the traditional gateway city offices. Out of the trio, only Park Place is classified as a Class-A building while both Diablo and Tanasbourne would better fit in the Class-B category.

Despite being seemingly lower grade buildings, the tenants are still Grade A tenants, most of which are listed and/or credit-rated. Examples are Toyota Motor’s financial arm, German-based Fresenius which is among the world’s largest providers of kidney dialysis products and services, Voya Services – formally ING U.S. after its spin-off and rebranding, and finally Nike with its core business in athletic shoes, apparel, and sports equipment.

Nike in particular rents the Tanasbourne campus for unique advertising studio reasons and not specifically as an office. The site is designed to allow Nike to bring in its sponsored athletes and celebrities discretely into its studio for greenscreen advertising photoshoots, away from the prying eyes of the paparazzi.

Source: Manulife US REIT

Pheonix, Arizona

Phoenix is the capital of the state of Arizona and the 11th-largest metropolitan area in the United States and one of the fastest growing in terms of population migration.

Tempe and Chandler – Education Power Houses

Tempe is among the premium commercial districts in Phoenix and is among the most expensive markets in the metropolitan area with average asking rents in the range of US$35 to US$40 psf. Tempe is anchored by Arizona State University (ASU) Tempe campus. Just west of Tempe is the Sky Harbor International Airport.

ASU, among the largest public education institutions in the U.S. by enrolment, is identified as one of the major factors that has fuelled real estate demand in the sub-market, supplying a large talent pool of highly educated STEM and TAMI talent annually. As a result, many high-profile tech and banking entities occupy premium quality assets in the area in order to attract these young talent. Examples of corporates setting up offices in Tempe include State Farm, Robinhood, JPMorgan Chase and Morgan Stanley.

Chandler on the other hand lies on the outer suburban area of Phoenix with lower average rentals than Tempe, approximately US$30psf on average. It benefits from the spill-over effects of office demand from Tempe, with many corporates in insurance, financial, semiconductor manufacturing and engineering looking to move some of their operations out of higher-cost markets.

More recently, Chandler has been a beneficiary of the chip shortage circumstances. Due to Arizona’s lower taxation, proximity to transportation nodes and a large talent pool in STEM, Chandler has emerged as a hub for semiconductor manufacturing.

Shifting Demographics with High Population Growth

JLL attributes this high growth of resident population to the low cost of living, lower state taxes, growing educated talent pool and warmer climate.

Since 2010, the resident population of Phoenix has grown by about 15.6% to 4.85mil. This phenomenal growth resulted in the residential population surpassing that of traditional gateway cities such as Seattle (4.02mil) and Detroit (4.39mil) and poised to overtake Boston (4.91mil) in the coming years. As the population expands, so will the needs for real estate in the office sector as corporates hunt for talent and the need to house an expanding workforce.

Phoenix is among the first major metropolitan district in the U.S. to recover and exceed the pre-pandemic employment levels. During the height of the COVID-19 pandemic, unemployment rate reached a high of 10.9% and that has since recovered to 3.8% as at the time of writing, according to JLL’s report (versus the national average for unemployment in the US of 4.6% as at the time of writing).

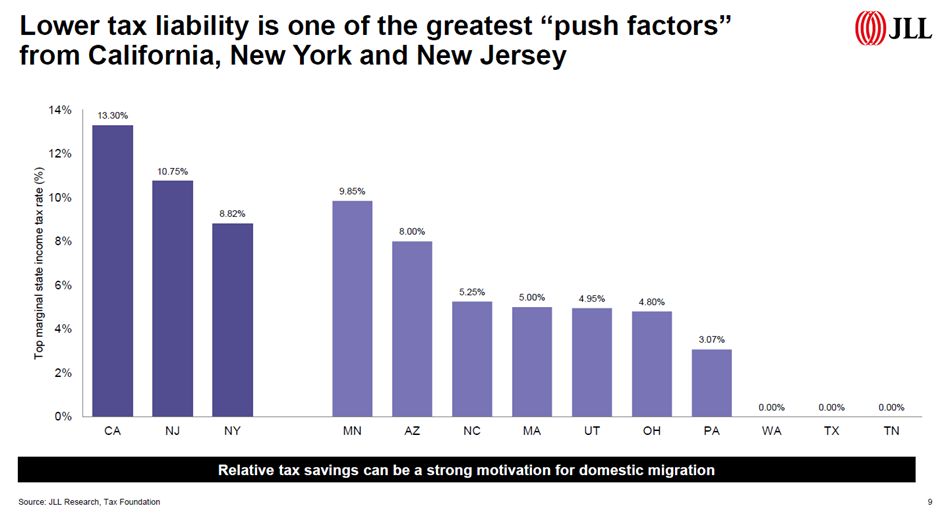

Part of the domestic migration into Phoenix is also attributed to lower tax liabilities which pushed talent out from neighbouring California down south to Arizona. California’s tax liabilities are estimated to be around 13.3%, while it is 8.0% in Arizona, according to JLL’s report in May.

Source: Jones Lang LaSalle (JLL) U.S.

Source: Tax Foundation

While tax is only one factor, a more significant factor to Arizona’s draw is its lower cost of living compared to its peer cities, specifically its cost of living ranking at #76 among major U.S. cities. For the purpose of comparison, New York City, San Francisco, Seattle, and Boston rank #1, #3, #6 and #8 in terms of their cost of living respectively.

Source: Jones Lang LaSalle (JLL) U.S.

Due to several factors such as milder and warmer weather, lower cost of living and lower taxes in Arizona, it has attracted the second most number of “California Refugees” to the state. According to the U.S. Census Bureau's annual American Community 2019 Survey, Texas (86,164 people) is the most popular destination for Californians moving out of state, followed by Arizona (68,516 people) and Washington State (55,467 people). It’s likely that these figures are much higher now post-COVID-19.

Significant population growth is a leading indicator for real estate rental demand and valuations. Coupled with a large talent pool and highly educated workforce, Phoenix will no doubt continue to attract technology companies and large corporates which will in turn drive up demand for high quality office and commercial spaces in the city.

One of the most notable examples of big tech companies making its way to Phoenix is on-demand food service DoorDash setting up its new headquarters in Tempe. It has cited similar factors shared above that make Phoenix an attractive place for it to sink its roots.

Portland, Oregon

While Portland is not the capital of Oregon (the capital is actually Salem!), it is the largest city in Oregon and the 25th-largest metropolitan area in the United States. While growth in population isn’t as fast as that of Phoenix, at 12.9% since 2010, it is much higher than the average of the gateway cities such as Chicago, Los Angeles, New York, Boston and San Francisco.

With approximately 40.3% of residents over the age of 25 having a bachelor’s degree or higher, Portland is home to an educated population. It is estimated that 47.6% of degreeholders in Portland have a STEM-classified major. This is significantly higher than the national average and roughly on par with gateway markets including New York and Chicago.

Among the office intensive corporations that have set up space in Portland are Intel, Providence Health, Nike, Kaiser Foundation, U.S. Bank and Wells Fargo. Combined, the ten largest office intensive employers employ a total headcountof 40,300.

Portland is also the headquarters of Nike. Besides Nike, other sports apparel manufacturers such as Adidas, Columbia Sportswear and Under Armour are also office intensive employers with a combined total of 1.5million sq ft across Portland.

Closing Thoughts

ProButterfly.com has never ceased to advocate that REITs should acquire new assets and real estate accretively and grow its shareholder value over time. MUST has done this well and the trio of acquisitions announced yesterday, with a 4.4% DPU accretion, is the most accretive acquisition MUST has carried out since its listing on the Singapore Exchange.

However, to us this deal marks more than just another accretive acquisition. More importantly, this marks the beginning of its diversification away from its long-standing strategy of targeting ClassA and Trophy assets in the traditional cities in the U.S.

The management has through this acquisition shown its nimbleness and flexibility by recognising the structural shifts in America’s domestic migration patterns and recentring its focus on the Sun Belt and emerging markets.

We hope that this growth strategy will continue well into the coming years when MUST shifts into high gear, and through multiple high accretion and high growth acquisitions generate a virtuous cycle of higher DPU, premium to NAV valuations and lower cost of equity as it continues its acquisition momentum.

This article first appeared on Probutterfly.com.